|

호텔 리스는 호텔 운영 및 부동산 보유시 수반되는 위험 부담을 낮출 수 있는 대안 중 한 가지로 1900년대 중반 처음 출현했다. 지난 20년간 호텔 업계 빅 4(메리어트, 힐튼, IHG, 아코르)는 매니지먼트 및 프랜차이즈 계약을 고수해왔지만 유럽 전역의 호텔 브랜드들의 관점에서 호텔 리스는 이미 매력적인 옵션으로 작용하고 있으며, 버짓 호텔 부문뿐만 아니라 슈테이겐베르거 (Steigenberger), 뫼벤픽(Movenpick), 델러타(Dalata)와 같은 풀서비스 호텔 브랜드들 역시 호텔 리스를 긍정적으로 고려할 것으로 예상된다.

최근의 세계 경제 판도에 따라 호텔 리스가 호텔 디벨로퍼와 오너 양측 모두에게 유리한 옵션이라는 점이 확인되면서 그 인기는 점차 높아졌다. 먼저 호텔 디벨로퍼의 관점에서 매니지먼트 계약시의 협상과 비교할 때 리스 계약 절차는 간단하다. 또한 비즈니스 모델 마련 및 운영에 따른 위험 부담을 줄일 수 있으므로 호텔 오너 역시 투자자들에게 이를 어필할 수 있을 것이다.

유럽 내 부동산 투자자들이 리스를 통해 부채를 활용할 수 있는 장기적이고 안정적인 수익 모델을 선호한다는 점을 고려할 때 자본 활용도가 높은 호텔 리스는 호텔 오너와 오퍼레이터 모두에게 유리한 옵션이라 할 수 있다.

매크로 트렌드와 마이크로 트렌드의 지속으로 고정 수입이 보장된 호텔에 대한 투자가 활발해짐에 따라 호텔 리스를 활용할 수 있는 최적의 시기가 이제 도래하게 된 것이다.

As one of the earliest forms of separating the risk associated with hotel operations and real estate ownership, lease contracts for hotels have been in existence since the mid-1900s. Despite the big four hotel brands (Marriott, Hilton, IHG and Accor) shifting to management and franchise contracts over the past 20 years, leases remain an attractive operating format in Europe for many other brands, especially in the budget segment, but also for full-service brands such as Steigenberger, Movenpick or Dalata.

The newfound popularity of leases within this economic cycle stems from the fact that they make a lot of commercial sense, for both developers and long-term owners. From a developer’s point of view, signing a lease contract is a relatively easy process (compared to negotiating management contracts) and, owing to the reduced risk associated with the operating business, provides a stable pool of forward-funding buyers.

Lease contracts create a similarly viable exit solution for owner-operators of existing hotels that wish to free up capital, as institutional real estate investors across Europe have a great appetite for long-term, secure income that they can use to match funds’ liabilities with inflation-linked leases.

With both macro- and micro-trends supporting fixed-income hotel investments, here are five reasons why there has never been a better time to structure hotel leases in decades:

호텔 오너와 디벨로퍼 모두 호텔 리스를 선택할 수밖에 없는 데는 다음과 같이 5가지 이유가 있다. Five Reasons Why Developers and Owners Love Hotel Leases

첫째. 오퍼레이터와 호텔 리스

Operators have a tremendous appetite to sign lease contracts

대부분의 호텔 브랜드들이 수년간 런던, 파리와 같이 세계 최대 규모의 시장에 국한하여 호텔 리스를 활용해왔지만 근래에 들어서 유럽 내 상당수의 오퍼레이터들이 2차, 하위 시장까지 판로를 확장하기 위해 호텔 리스를 활용하기 시작했다.

영국의 프리미어 인(Premier Inn)이나 독일의 모텔 원(Motel One)과 같은 버짓 호텔의 오퍼레이터들은 장기적으로 안정성이 확보된 고정형 리스를 바탕으로 리스크를 최소화하기 위해 호텔 리스를 선택하는 것으로 나타났다. 또한 프리미어 인의 허브(hub by Premier Inn), 이지 호텔(easyHotel), 노코(NoCo)와 같은 버짓 브랜드들이 객실 수를 증가시켜 시내 중심지역의 ㎡당 수익을 극대화하기 위해 작은 크기의 객실 공급을 확대하고 있는 것도 이들이 리스를 선택하는 이유이기도 하다.

버짓 브랜드뿐만 아니라 상당수의 업 스케일 호텔 오퍼레이터들의 리스 선호도 역시 증가하고 있다. 조사에 따르면 시티즌 엠(citizenm)이나 25 아워스(25 hours)와 같은 업 스케일 브랜드들은 장기 운영 계약에 앞서 브랜드의 콘셉트를 효과적으로 증명하기 위한 방법으로써 호텔 리스를 선택하는 것으로 나타났다. 이 경우 투자자들은 자산을 보다 다양화하고 호텔 자산 전반에 작용하는 리스크를 감소시킬 수 있다.

While brands have been forced to sign lease contracts to expand into the most high-profile locations of London or Paris for decades, several operators are now willing to expand outside of these ultra-prime locations to primary and secondary markets across Europe.

Budget operators, such as Premier Inn in the UK or Motel One in Germany, more commonly sign lease contracts, as they benefit from a low-risk operating model that enables them to take on long-term, index-linked fixed leases. Additionally, many budget brands are expanding concepts with smaller room sizes (for example, hub by Premier Inn, easyHotel or NoCo) which allow them to fit more beds in the same amount of space and thus maximise revenue per m2 in city centre locations.

In addition to budget brands, a number of upscale operators with a long-term view of expanding into management contracts are increasingly taking on leases as a way to initially prove their concept, with successful examples over the past decade including citizenM or 25hours hotels. As an added benefit to investors, these alternative brands allow portfolio managers to diversify their holdings and mitigate risk across hospitality assets.

둘째. 기업 투자자와 호텔 리스

Very low exit risk for developers as institutional investors buy into hotels

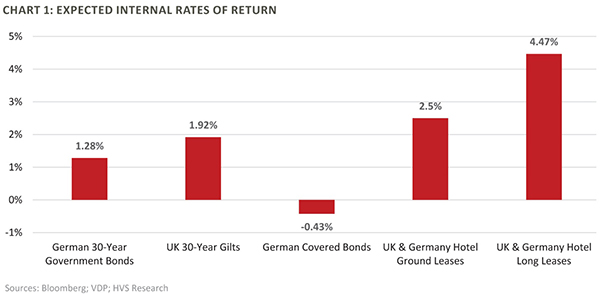

수익률이 낮은 동시에 인플레이션의 리스크도 과거보다 낮아진 글로벌 거시 환경이 갖춰지면서 기업 바이어 입장에서 호텔은 매우 매력적인 투자처가 되었다.(표 1 참고) 연금 펀드와 보험사, 기타 고정 수익 투자자들이 국부 펀드로부터 기대 수익을 얻지 못하면서 호텔 투자로 관심을 돌리기 시작했다. 2016년 한 조사에 따르면 리스 호텔의 개인 투자자 수가 높게 나타나면서 리스 호텔에 대한 투자 선호도가 증가한 것이 입증되었다.

이와 같이 리스 호텔 투자가 지속적인 오름세를 보이고 매체의 진보에 따라 호텔 투자 시장이 투명해지면서 기업 투자자들은 리스 호텔 투자를 늘리고 더 나아가 호텔 시장의 가치를 높게 평가하게 되었다. 또한 투자자들이 성장하고 투자 패턴이 다양해지면서 리스 호텔을 고위험군으로 분류했던 투자자들 역시 이를 수익 창출의 기회로 재고하기 시작했다. 실제로 국제회계처리기준인 IFRS 16이 2019년부터 발효됨에 따라 매출 기반 리스 모델 등이 출현하면서 버짓 부문 외 브랜드에 대해서도 투자가 증가하기 시작했다.

Given the global macro environment of low yields and the reduced risk of inflation, hotels have become a very attractive investment opportunity for institutional buyers (as shown in Chart 1). As pension funds, insurance companies and other fixed-income investors are unable to get their required returns from sovereign bonds, they are increasingly interested in hotels as an asset class. This interest is also demonstrated by the record number of individual buyers investing in leased hotels in 2016.

As these factors continue to attract capital in the future and the hotel investment space becomes more transparent through the availability of data, institutional investors will most likely continue to invest in leased hotels and further commoditise the market. As the pool of investors grows and the cycle advances, those investors that have been considering leased hotels for the longest time might also start exploring deal types they have previously deemed too risky. Examples include investments outside of the budget sector, accepting turnover-based rent structures or shortfall caps on guaranteed rent levels which many tenants are using as a reaction to IFRS 16 accounting standards taking effect in 2019.

셋째. 고정 수익 호텔 시장 내 변화

Hotel capitalization rates are at historical lows

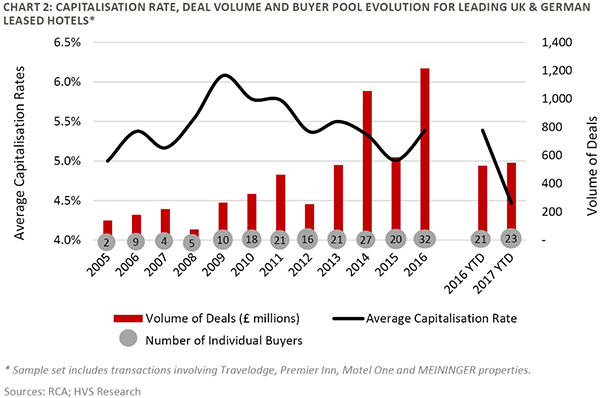

최근 몇 년간의 자본화율 변동 추이에 따라 고정 수익과 리스 호텔 투자 선호도가 증가한 것이 확인되었다. 물론 공실 수익이 소폭 증가하고 운영 계약에 따른 수익 역시 지난 조사 최고치와 동일한 수준인 것으로 확인되었으나 고정 수익 호텔의 경우 지난 해 수익을 넘어서면서 변화가 가장 크게 나타났다.

유럽 내 고정 수익 호텔 시장 중 가장 성숙하고 투명한 시장은 영국과 독일이다. 2017년 제 3분기까지 이들 시장 내 하이클래스 리스 호텔의 수익은 약 4.5%에 달했으며,(표 2 참고) 이는 지난 해 주당 순자산가치 최대치 대비 50배에 상당하는 수치인 것으로 확인되었다.

The investment appetite for fixed-income, leased hotel investments is also evident in the compression of capitalisation rates over recent years. Although vacant possession yields are slightly above, and management contract yields have equalled those of the peak of the previous cycle, fixed-income hotel yields have surpassed any previous records.

As the UK and Germany are the most advanced and comparatively the most transparent fixed-income hotel markets in Europe, these provide a good comparison to the previous cycle. Looking at these markets, by the third quarter of 2017 (as shown in Chart 2) prime hotel lease yields have reached circa 4.5%, which is approximately 50bps below the peak of the previous cycle.

넷째. 다양한 리스의 출현

Room for additional value creation with sandwich leases and ground leases

지난 10년 간 유럽 시장에 자리를 잡은 써드파티 오퍼레이터들은 호텔 리스를 활용하는 한편 메이저 호텔사와 프랜차이즈 계약을 체결하여 자산을 브랜딩하는 방식으로 유연성을 갖추었다.

제 3의 개인 투자자나 기업이 투자하고 운영은 아웃소싱하는 형태의 “샌드위치 리스” 또한 점차 증가하고 있다. 일각에서는 이러한 샌드위치 리스를 고위험군으로 분류하기도 하나 호텔 디벨로퍼 입장에서는 투자 부담 없이 운영 가능한 모델이라는 점이, 건물주 입장에서는 운영 실패에 따른 손해율이 낮다는 점이 장점으로 작용할 수 있다.

상업용 부동산 중 토지만 임대하는 그라운드 리스(Ground lease) 혹은 만기 인수형 장기 리스 역시 개발 초기 단계에서 자금을 확보할 수 있다는 점에서 디벨로퍼로서 고려해볼 수 있는 옵션들이다. 이러한 만기 인수형 장기 리스 모델의 경우, 향후의 자산 소유권자는 합리적인 금액(예상 EBITDA 기준 최대 20%)으로 그라운드 리스를 활용하고 장기적인 관점에서 호텔을 담보로 자금을 운용하는 이점을 취할 수 있게 된다. 이러한 수익 모델들은 건물 자체의 수익성을 높이는 데에 기여하는 동시에 디벨로퍼의 자금 부담을 완화하여 향후 추가적인 가치를 이끌어낼 기반으로 작용할 수도 있는 것이다.

As third-party operators took a foothold in Europe over the past ten years, they brought added flexibility to the fixed-income hotel investment scene by also committing to leases, while branding their properties through franchise contracts with one of the major hotel companies.

A similar structure coined as ‘sandwich leases’, whereby the third party is committed to the lease, but outsources management through a management contract, has also become more commonplace. While considered relatively risky, the structure can create value for developers as a non-investment grade management contract or tenant can be made institutionally accepted this way, unlocking an end-investor base with a much lower cost of capital.

Another form of unlocking value for developers is through ground leases or income strips, whereby developers sell the land early in the development process as an alternative to development financing. These income strips subject the future owner of the property to an affordable ground lease payment (usually up to 20% of projected EBITDA), and are valued at lower yields as they are often very long term and heavily collateralised by the underlying hotel. While this structure does increase the yield on the building itself, the lower-yield ground portion and the decreased financing costs can help developers unlock additional value.

다섯째. 금리 변동에 따른 투자 선호도 변화

Interest rates are set to rise in the medium term

미국 내 금리가 오름세를 타고 영국 금융 시장에도 변화가 일면서 고정 수익 호텔에 대한 투자 가치가 지금보다 더 높아지리라 장담할 수 없게 되었다.

전문가들에 따르면 유럽 내 금리는 2019년까지 꾸준히 인상될 것이며, 수반되는 금융 비용 증가에 따라 호텔의 자본화율에 대한 압박 역시 크게 증가할 것으로 예상된다. 물론 이러한 금리 인상에 따라 일부 기업 투자자들이 국부 펀드로 다시 눈을 돌릴 수 있다. 그러나 호텔 펀드에 대한 투자가 다른 자산에 대한 투자 대비 규모가 작은 만큼 투자자들의 호텔 투자 선호도는 소폭 하락하는 데서 그칠 것으로 보인다.

As interest rates in the US are already on the rise, with the UK anticipated to follow having just embarked on this journey, the environment for fixed-income hotel investments cannot be realistically expected to remain as favourable as it is today.

Analysts expect gradual interest rate rises across Europe from 2019, which arguably will place upward pressure on hotel capitalisation rates as financing costs increase. The same interest rate rises will also push institutional investors back towards sovereign bond investments; however, it could be argued that as hotel fund allocations are still relatively low compared to other asset classes, institutional investor interest for hotels will not decrease substantially.

마무리 Conclusion

장기적인 리스 계약을 체결하기 위한 오퍼레이터의 노력과 적시에 자금을 조달할 수 있는 투자자의 자산, 니즈에 맞는 호텔 프로젝트, 이 세 가지가 아우러지면서 고정 수익 호텔 시장은 그 어느 때보다 호황을 누리고 있다. 자산 가치를 높게 평가받는 호텔이 점차 증가하고 있다는 사실을 고려할 때 호텔도 궁극적으로는 유동자산이라는 점은 그 어느 때보다 중요하며, 적시의 투자 결정, 리스 비용 조달, 호텔의 향후 수익률에 대한 충분한 이해가 이루어진다면 프로젝트가 창출해낼 수 있는 최고의 수익을 이끌어낼 수 있을 것이다.

To conclude, operators’ willingness to commit to long-term indexed lease agreements and investors’ readiness to buy as well as forward-fund hotel projects has enabled the fixed-income hotel market to become far more commoditised in this cycle than ever before. While hotels being accepted as an asset class of their own has benefited the hotel industry, investors and developers should be conscious of the fact that hotels are ultimately trading assets. With this in mind, well-timed investment decisions supported by professional advice on lease term negotiations, rent coverage and a thorough understanding of the hotel’s future income producing ability should ultimately enable investors to extract the most value from each project.

| |

|

|

| |

Peter Szabo

Peter Szabo is an associate at HVS Hodges Ward Elliott, having previously worked at Horwath HTL’s Budapest office. His primary responsibilities include financial analysis, development of marketing materials and due diligence. Peter is a native Hungarian speaker and also speaks German.

|